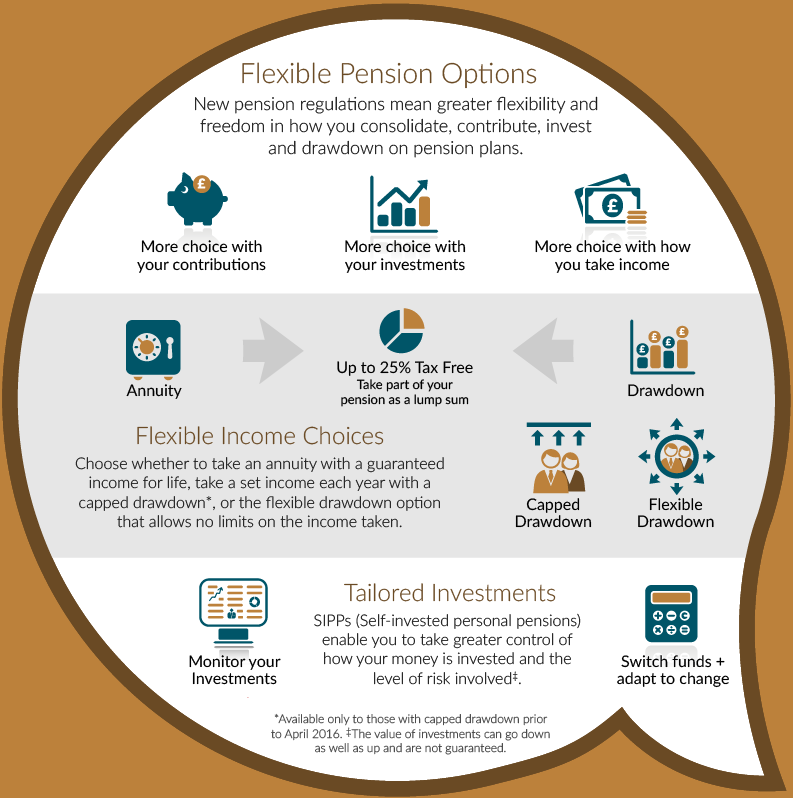

SIPPS: At a Glance

Self-invested personal pensions (SIPPs) offer a flexible approach to pension schemes, enabling complete control over how your pension is invested, and more choices as to how you use your pension in retirement.

- Wider investment choice with access to 1000s of funds, shares and trusts

- Greater flexibility, control and access to your pension

- Available in annuity or drawdown

- Greater opportunity to make better returns, though at greater risk